Overview

OverviewConsumers rank certainty and flexibility as the two most important features when planning their retirement1. However, the choice is usually presented as a binary decision – the flexibility of drawdown or the certainty of a lifetime annuity. But is there a special alchemy when the two solutions are combined?

Hybrid or integrated solutions haven’t yet gained significant traction. Is this unsurprising? A common benefit is often cited as the ability to cover essential expenditure with a guaranteed income. But how relevant is this to affluent clients? As income increases the proportion of the household budget required to cover essential expenses decreases. The wealthiest households spend around 15% of their income on housing, fuel and power compared with almost 28% of the income of the poorest households2.

Many affluent clients are likely to have a full State Pension, and perhaps some defined benefits, so the need to use a lifetime annuity to cover any shortfall is limited. Nevertheless, this is not the only reason to adopt an integrated solution.

Let me count the ways…

The interaction between drawdown and a guaranteed income creates a powerful synergy:

- It’s not just about essential expenses

For more affluent clients, retirement isn’t just about surviving. These people often have ambitious goals. This may include fees to an exclusive golf club, extensive overseas travel or expensive new hobbies. If this is important expenditure it may make sense to cover this with a guaranteed income stream. Adding this to essential expenditure may require more guaranteed income than the State Pension and any defined benefit income provide. - A hybrid approach can deliver better outcomes

A 2018 study by actuarial consultants, Milliman, showed that replacing the bond element of a drawdown portfolio with a lifetime annuity could be beneficial. The example in the chart below shows how an annuity-equity strategy produces a safe withdrawal rate of 3.3%, compared with 3.1% from a bond-equity strategy over a 30 year period.

Sustainable withdrawal rate (increasing with inflation) for healthy 65-year-old female, fund: 55% equity, 5% cash, 40% bond or annuity

Source: Annuities reinvented: Are annuities the missing asset class for sustainable drawdown solutions? Milliman, 2018.

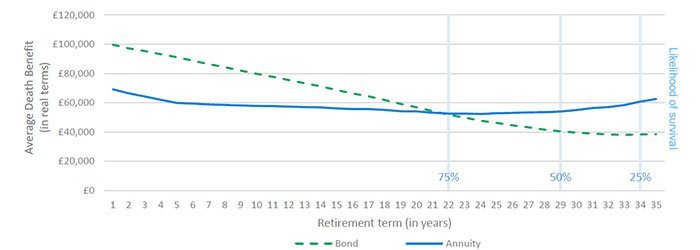

That’s not all. The analysis revealed that the annuity-equity and bond-equity strategy differ in terms of the level of death benefit they could provide. Over the long term, the annuity-equity strategy can provide a higher death benefit.

Average death benefit for healthy 65-year-old female, target income of £4,000 a year (increasing with inflation). Fund: 55% equity, 5% cash, 40% bond or annuity (5-year guaranteed period)

Source: Annuities reinvented: Are annuities the missing asset class for sustainable drawdown solutions? Milliman, 2018

There is a logic behind this. Firstly, the higher income from an annuity (compared to the bond element), means less needs to be withdrawn from the drawdown fund to provide a given amount of income. Secondly, the bond-equity strategy is rebalanced each year but, as annuities can’t be bought and sold, the annuity-equity strategy is not rebalanced.

The Institute and Faculty of Actuaries also modelled a range of strategies involving drawdown and annuitisation and concluded that by adopting an integrated strategy ‘consumers can potentially generate a larger overall income from their pension pot’3.

- A hybrid approach can also help combat sequencing risk

Consider a 65 year old with a £500,000 fund planning to withdraw 4% each year. Using £200,000 to buy a single life level annuity would provide over £14,000 each year4. That means the client only needs to withdraw under 2% from the remaining £300,000 drawdown fund, so less has to be disinvested each year or set aside as a cash bucket. This is based on a level annuity, so inflationary increases would need to be provided by the remaining fund. - Tax advantages

There are potential tax advantages if an annuity is included as a drawdown asset:- If the income from the annuity isn’t needed at any point, it is added to the drawdown pot. If the annuity is written separately, it would be taxed as income. This could be useful for someone who wants to take advantage of high annuity rates, but is still working so doesn’t need the income.

- On death after 75, there is scope to take lump sum death benefits, like value protection, from an annuity written under drawdown as a regular income, which might be taxable at a lower rate than if death benefits were payable from a separate annuity (the treatment of death benefits is set to change from April 2027).

The FCA raised the need to consider annuities in its thematic review. An integrated solution can provide the certainty of income from an annuity with the flexibility of drawdown. Perhaps the best of both worlds?

You can discover more about this subject in our report Investment risk and retirement.

Latest articles

Pensions: The regulatory runway

What pension changes are coming?

Marianna Hunt

Fidelity International

25 February 2026

Evolving stability: smoothed funds reimagined

Trying to shield policyholders from the extremes of market volatility isn’t a…

Andy Brown

Head of Fund Solutions at Standard Life

28 January 2026

Tax increases reignite the bonds versus collectives question

Tax hikes on savings and dividends from 2026 and 2027 slightly shift rates bu…

Paul Squirrell

Head of Retirement and Savings Development

21 January 2026